|

|

posted: April 6, 2018

tl;dr: Insurance companies can lie with impunity, except (hopefully) in a court of law...

See part one for an explanation of the fundamental issue: the diminished value a vehicle has once it appears on an accident report, even if the damage is minor.

Picking up the storyline: I did file a claim with the Illinois Department of Insurance, the state insurance regulator. I figured I should do that before hauling Sentry Insurance into court, lest the court case be thrown out because I had omitted that step. Fortunately this was a fairly easy process, all on-line: I didn’t have to visit a state office building. I did have to fill out online forms and assemble and scan lots of other paperwork as evidence.

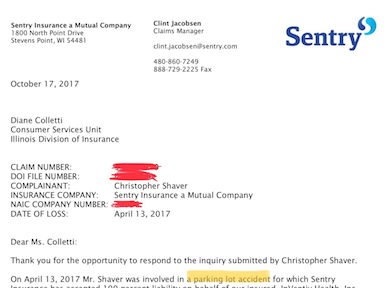

Sentry’s response to the inquiry from the state was ludicrous and contained some fresh new lies to compound their other lies about how my vehicle has not lost any value because of the accident report. Amazingly, in the second sentence of their letter they stated that “Mr. Shaver was involved in a parking lot accident”, in direct contradiction to the police crash report and the facts: the accident happened on a major road when a high-speed distracted driver slammed into the vehicle behind my Jeep, pushing that vehicle into my Jeep. Sentry basically tried to convince the state insurance regulator that the accident was a minor parking lot fender bender, and that I was trying to scam them for much more than I was due. They even claimed that the repaired vehicle might have a higher post-accident value than pre-accident, since “the replacement of these parts should appeal to buyers, not deter them”. Then to top it off they stated that my “allegations that representatives from Sentry have ‘repeatedly lied’ to (me) are false”. Who is the state supposed to believe: a reputable insurance company or a possible scam artist making a big fuss about a parking lot accident?

|

|

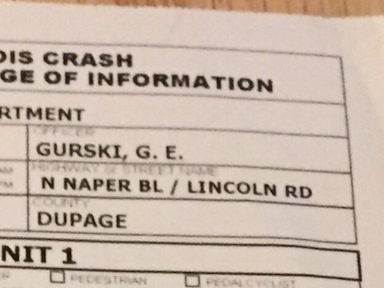

The police and Sentry Insurance don't quite agree where the accident occurred...

Fortunately for me this was a major tactical blunder by Sentry. The state refused my claim not because of anything that Sentry said, but because “only a court of law has the authority to determine diminished value on a vehicle”. The state regulators simply lacked jurisdiction. Sentry could have remained silent except to point out this fact; instead they gave me more evidence to use against them in court. In my dealings with their personnel, it is clear that I’m not dealing with highly intelligent people. Sometimes I feel a little guilty taking advantage of people’s stupidity, but not in this case.

The big lesson from the episode with the state is that insurance companies will blatantly lie to state regulators. I guess I shouldn’t be surprised about this, as they are not under oath to tell the truth. I was expecting a higher standard of ethical behavior, because insurance companies have great power: by themselves they determine how much to pay out in claims, and the only recourse is to haul them into court. which is a long, involved process. Sentry was obviously betting that I wouldn’t do this, which only gave me more motivation to do so. I’ve now filed in Small Claims Court and served the summons on the company.

Sentry is a mutual insurance company, meaning that it is supposedly run for the benefit of the policyholders, not external shareholders. Perhaps that is part of the problem: Sentry is not my insurance company, it is the insurance company of the criminally negligent distracted driver who caused the accident. It is to the benefit of that distracted driver that Sentry pay me as little as possible, so that it can keep rates low for the distracted driver in the future. But Sentry may refuse to write a policy for that driver in the future; if I was them that’s what I’d do.

Sentry’s behavior demonstrates that the company really is being run for the benefit of the people who work at the company, who get nice fat salaries in a low cost-of-living city (the headquarters are in Stevens Point, Wisconsin), who get to work in cushy 9-to-5 jobs with little turnover, and who get to golf at the company’s golf course and attend PGA tournaments sponsored by the company. The only way to win at the insurance game is to work for an insurance company or to own part of one; everyone else either pays more to the insurance company than they get in return, or in the case of a serious injury or health problem or loss that the insurance company actually covers, they have to suffer because of the problem causing the claim. The only true winners are the insurance company employees and shareholders. I am seeing first hand why Warren Buffett likes owning insurance companies.

Meanwhile, I’ve got a court date coming up...

Update: see part three