|

|

posted: June 7, 2020

tl;dr: How badly do you have to fail Econ 101 to buy a negative yield bond?...

Disclaimer:

The information contained in this post is not intended as, and shall not be understood or construed as, financial advice. I am not a financial advisor, accountant, or attorney, nor am I holding myself out to be. The information I present is not a substitute for financial advice from a professional who is aware of the facts and circumstances of your individual situation, which is different from my own. You should seek the advice of a financial professional who is capable of understanding your own personal situation, your goals and aspirations, and making recommendations suited to you.

Earlier in my lifetime it was possible to save up money for future expenses. The money you deposited in a passbook savings account would grow through “the miracle of compound interest”. If you wanted to earn a higher interest rate and didn’t mind locking your money up for a fixed time period, you could easily buy a Certificate of Deposit (CD) from a bank or savings and loan. CDs actually paid decent interest rates plus they were federally insured, meaning the risk was nearly zero.

I was able to save up a portion of my college expenses at Cornell by banking the money I earned in high school, some by working as a programmer for a startup. Even though inflation was high in the late 1970s and early 1980s, so were the interest rates paid to savers. The 30-year Treasury yield curve in the I sold my bonds post is roughly equivalent to CD interest rates, since one way for banks to pay interest on CDs is to pool them and buy a Treasury bond. CDs in that era sometimes yielded in the double digits: I seem to recall one CD I bought that paid 16% a year. College tuition was not (yet) rising that fast. So believe it or not, it was possible to earn money, put it in the bank, and receive money in the future that had more college tuition purchasing power than at the time of deposit. This sure beat taking out student loans: I never had to do so.

Those days are long gone. Interest rates have plunged and college tuition has skyrocketed. Savers are punished by low interest rates, and have to take on more risk in order to earn a decent return. For borrowers, life is great. It is so great that some borrowers, such as the governments of Japan, Germany, and France, are able to unload bonds that have a negative yield, meaning the lender pays interest to the borrower. The current U.S. president has proposed negative yields for this country’s bonds. This brings up a question I struggle to answer: who in their right mind buys a negative yield bond? Governments can try pricing their bonds wherever they want, but if they can't find a sucker willing to buy a bond that's going to lose money, they won't be able to sell it.

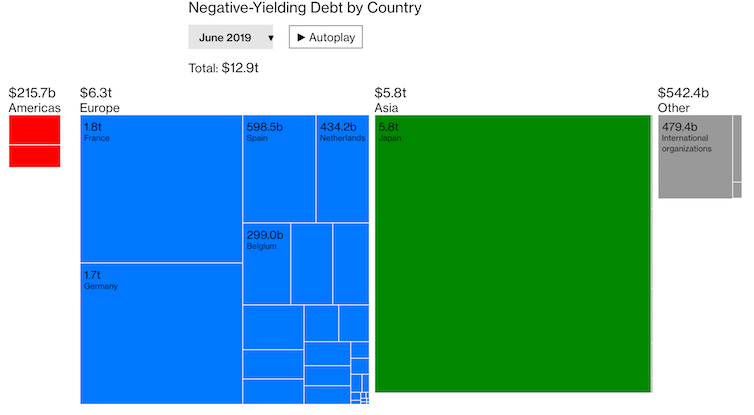

From Bloomberg: in mid-2019 nearly $13 trillion dollars of bonds have been purchased by people who don’t mind losing money

The Bloomberg article that I got the graphic from doesn’t answer the question. It even states that “persistent fears of deflation — falling prices — can make negative yields seem like a reasonable deal.” That doesn’t make sense because one alternative to buying a negative yield bond, whether there is deflation or inflation, is just to hold the currency in which the bond is denominated. You don’t get any interest, but you also don’t lose any money. You also give yourself the option of investing in something else in the future.

Small investors can easily hold cash in a bank with federal deposit insurance. Larger investors have some minor challenges holding onto large amounts of cash. They might have to take physical possession of the cash, in large denomination bills, and figure out a safe place to store it, over a long period of time, so that it cannot be stolen. Storage, transportation, and security costs will be incurred. A slightly negative yield bond might be equivalent to the costs of holding onto large amounts of cash, which is one reason why a large institution might buy a negative yield bond.

Some negative yield bonds might be being purchased by bond funds on behalf of investors who don’t realize what is going on. A large amount of money flows into the stock and bond markets every month because of worker's 401(k) contributions, which are typically set up as fixed allocations to a variety of funds. Some workers with 401(k)s may have chosen conservative bond funds, whose charters state that they must invest in safe government-issued bonds. So if the yields for those bonds dip into the negative, the 401(k) contributions continue to flow into the bond fund, which now has to buy negative yield bonds. Investors may not realize they are losing money, and change their allocations, until much later. Or the negative yield bonds may be blended together in the fund with other positive yield bonds, such that the overall return is slightly positive. The investor may be happy with that level of performance.

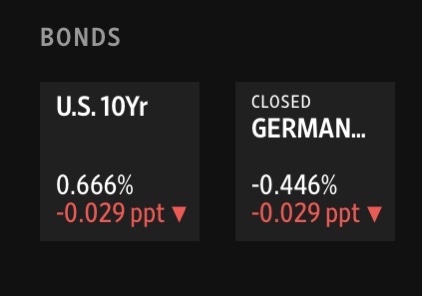

10 Year government bond yields as of May 29, 2020, from Wall Street Journal

German bonds, which are issued by Germany and are denominated in euros, often have the most extreme negative yield among all the negative yield bonds. There’s a possibility that some purchasers of these German bonds are betting that the European Union (EU) fractures over the holding period of the bond. If the EU fractures to the point that countries disband the euro and replace it with their own national currencies, the holders of German bonds would have them converted into Deutschmark denominated bonds. German central bankers, by tradition, are fearful of inflation, and probably would manage the Deutschmark to better maintain long term value than the managers of the euro, the European Central Bank. The expectation of ultimately returning to a stronger currency, the Deutschmark, could explain why some investors are willing to buy negative yield German bonds today.

The greater fool theory may also be at work. This theory states that it doesn’t matter what price you pay for an asset, as long as someone in the future (the greater fool) decides to buy that asset from you at an even higher price. So a German 10-year bond that yields -0.446% might make the purchaser some money if interest rates go even further negative, say to -1.000%. A greater fool might show up to buy your -0.446% bond because it loses less money than a -1.000% bond, and the purchaser really needs to own a German bond for the other reasons mentioned above.

Those are the only reasons I can think of for buying a negative yield bond. As I already mentioned, I sold my bonds. I know too much economics and math to buy a negative yield bond.

Related post: Who would buy a negative real yield bond?

Related post: The end of the bond market

Related post: Prices can rise when demand falls