|

|

posted: June 5, 2021

tl;dr: How badly do you have to fail Econ 102 to buy a negative real yield bond?...

Last year, when consumer price inflation was still low but, I believed, headed much higher due to the COVID-19 pandemic, I sold my bonds. At the time, I was flabbergasted by the amount of money being lost, in nominal terms, by bonds with negative interest rates, and wondered who would buy a negative yield bond, especially when the alternative of holding cash exists? Now, with inflation as measured by the U.S. Consumer Price Index (CPI) having revved up to an annual rate of 4.2% in April 2021, bond yields have risen a little. There are fewer negative yield bonds being sold worldwide, although the Germans are still able to do so. Yet the “real” yield, which takes inflation into account, for many bonds is even more negative than a year ago, especially for short-term bonds. Who is buying these negative real yield bonds?

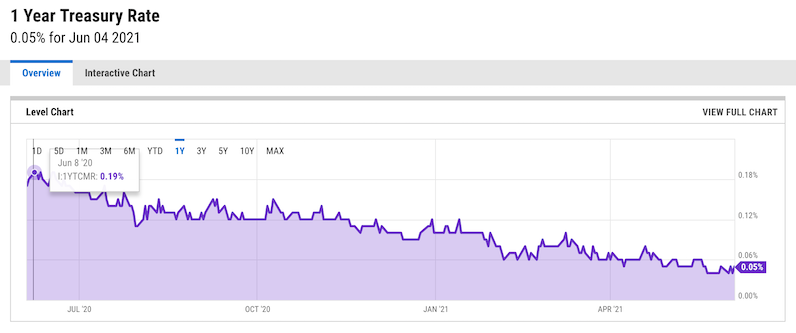

A stark example is the one-year U.S. Treasury bond or T-bill (short-term bonds are also called “bills”). We can look back in time to see what happened to people who bought a one-year T-bill one year ago. One year ago, after the onset of the pandemic, the one-year T-bill yielded around +0.2% of interest. A $10,000 T-bill bought in April 2020 returned about $10,020 in April 2021. Yet because of inflation, the basket of goods in the CPI calculation, which cost $10,000 in April 2020, cost $10,420 in April 2020. The one-year T-bill buyer lost $400 of purchasing power.

Amazingly, with inflation revving up, the yield on the one-year T-bill has actually declined, to a current yield of 0.05%. Inflation forecasting isn’t a perfect science, but is there anyone who thinks that consumer prices won’t rise at least 0.05% over the next year? I daresay that everyone who is buying one-year T-bills at the current nominal yield of 0.05% knows that these bonds will have a negative real yield, and that they will lose purchasing power.

A 1-year Treasury purchased a year ago yielded under 0.2% (source: YCharts), while CPI increased 4.2%

Parking the money in cash is a solution to negative nominal yields, but doesn’t work in this negative real yield situation. At least the 0.05% T-bill will turn $10,000 into $10,005 in a year’s time. But who is buying these bonds, which are all but guaranteed to destroy purchasing power?

One set of buyers is the same as was described in my post on buyers of negative yield bonds: institutions who absolutely have to purchase bonds, regardless of yield, because of the very structure of the institutions and the safety factor of government-issued bonds. These are the captive buyers. Institutions such as pension funds, retirement funds, banks, insurance companies, and corporate treasuries buy bonds when they take in cash, mostly for safety and liquidity reasons. It may even be written into their charters that they must invest a certain percentage of available capital in bonds. No matter what the nominal or real interest rate, whether positive or negative, they buy bonds. While this may appear to be foolish to some people, some of those people may have money that is managed by these yield-insensitive bond-buying institutions without even realizing it.

An individual might knowingly buy a negative real yield bond if that person cannot yet decide what he or she wants to buy with the money, or wishes to defer the purchase. An example might be next year’s college tuition for a child. If the tuition can be prepaid a year in advance at the current price, which is almost certainly going to be lower than next year’s price, it’s better to buy it now. But that may not be possible, in which case the person might buy a one-year T-bill and accept the loss of tuition purchasing power. Thanks to the negative real yield T-bill, the purchaser will be forced to come up with even more tuition money in a year.

Another category of buyer is someone who is pessimistic on what he or she wants to buy, such as stocks or real estate, and thinks the market will go down over the next year even as CPI goes up. Asset prices have gone up much more than consumer prices since the onset of the pandemic, and those asset prices may come crashing back down. Someone who believes this is likely might park money in a one-year T-bill, wait for the crash, then swoop in and use the T-bill proceeds to pick up the desired asset(s) at lower prices. In this case, because they are planning to use the money to invest in assets rather than consumer goods, it doesn’t much matter that the T-bill has a negative real yield.

The final category of buyer is the most important one: the Federal Reserve. As part of its latest quantitative easing program, the Federal Reserve has been buying $80 billion a month of Treasury bonds. A good portion of those bonds, no doubt, are negative real yield T-bills. The Federal Reserve buys bonds with money that it itself creates, and it does not matter at all if the Federal Reserve ultimately makes a positive or negative return on these bonds. So the Federal Reserve keeps buying, to inject money into the economy and to keep interest rates lower than they would otherwise be. When you can print the money to buy anything, you don’t much care what the price is.

Related post: Who would buy a negative yield bond?

Related post: The end of the bond market

Related post: Look out below!