|

|

posted: July 31, 2021

tl;dr: The real returns on the major financial asset classes that most people use to grow their savings are all now negative...

The information contained in this post is not intended as, and shall not be understood or construed as, financial advice. I am not a financial advisor, accountant, or attorney, nor am I holding myself out to be. The information I present is not a substitute for financial advice from a professional who is aware of the facts and circumstances of your individual situation, which is different from my own. You should seek the advice of a financial professional who is capable of understanding your own personal situation, your goals and aspirations, and making recommendations suited to you.

I suppose it was inevitable that the COVID-19 pandemic would cause a major hit to the global economy and destroy wealth. As someone with a modest amount of financial education, knowledge, and experience, it’s been fascinating to watch this process unfold. It’s far from over, and it is happening in a way that few people realize. Many people actually feel pretty flush, thanks to government stimulus checks and 401(k) balances increasing as the stock markets post new all-time highs. Wages are also rising.

The culprit is inflation. When you adjust all these figures for inflation, a far different picture emerges. With the Consumer Price Index rising at 5.4% year-over-year, a dollar today buys less, on average, than what 95 cents bought a year ago. Wages are growing at between 3% and 4% year-over-year, which is less than inflation, so real (inflation-adjusted) wages are falling.

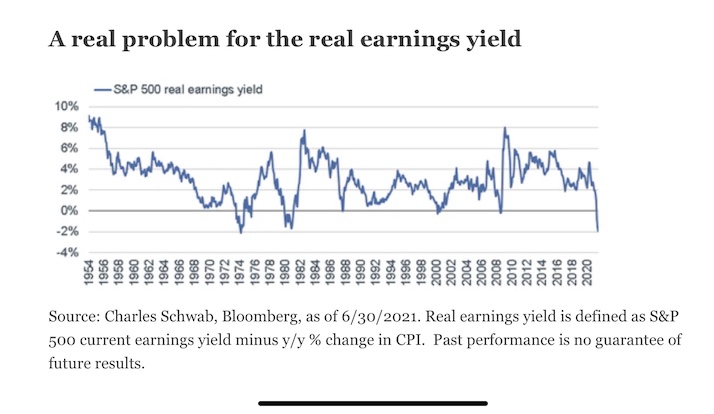

It’s easy to see that real bond yields are negative, a topic I covered in Who would buy a negative real yield bond? What shocked me this week is this chart, which was tweeted out by Liz Ann Sonders, the Chief Investment Strategist for Charles Schwab & Co., Inc.

S&P 500 real earnings yield

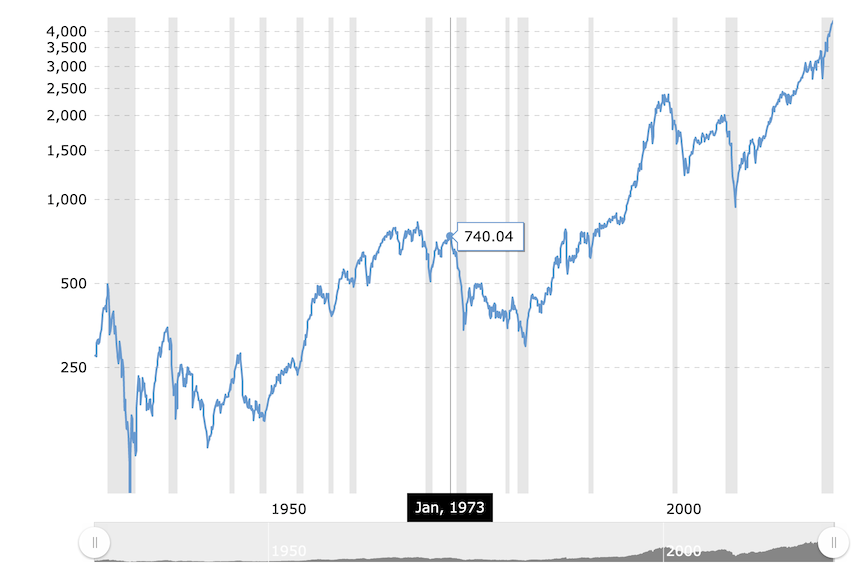

With inflation having risen, the real earnings yield for the S&P 500 has entered negative territory. Even more shockingly, every time the S&P 500 has done this over the past 70 years, the stock market has crashed soon thereafter. The stock market has crashed without the real earnings yield going negative, so it doesn’t predict all crashes, but every time the real earnings yield has gone negative, the market has crashed. You can use this chart to see what the S&P 500 has done over this timeframe:

S&P 500 price chart, log scale, from Macrotrends

In short, the stock market crashes within a year or two of the earnings yield going negative, which returns the real earnings yield back into positive territory.

The earnings yield is important for old-school value investors like myself; it matters not at all to momentum investors. Stocks are ultimately claims on the future cash flows from a business. Those cash flows primarily come from earnings; the stock price in the long run should be the discounted value of all future cash flows. A stock trading at $80/share which posts earnings over the past year of $2/share has a Price/Earnings ratio (P/E) of 40. The earnings yield is the inverse ratio, E/P, which in this example is $2/$80 or .025 or 2.5%. With inflation above 5%, that 2.5% yield isn’t yielding enough earnings to keep up with the devaluation of the currency: the real earnings yield is negative. If the stock price crashes from $80 to $33, the earnings yield is $2/$33 which is 6.1%, which would be above the inflation rate, so the real earnings yield would again be positive. The real earnings yield could also go back positive if inflation is quickly extinguished, or if earnings grow much faster than inflation and the stock price remains roughly flat. History, however, says that a crash is what does it.

With inflation running hot, the Federal Reserve suppressing interest rates, and the stock market having risen to the point where P/E is high and earnings yield is low, we’ve now reached the point where:

We appear to be heading off the cliff...look out below!