|

|

posted: April 13, 2019

tl;dr: The multiple reasons I sold my small piece of Illinois at a loss...

Part Two of a three part series on why I joined the Illinois Exodus

Part One: Death by property taxes in Illinois

Part Three: Illinois property tax scams

I’ve never, ever viewed the house I live in as an “investment”; “money pit” is the phrase that instead springs to my mind. I've written another blog post on all the ways you are going to lose money on the home that you own and occupy (hint: the difference between the purchase and selling prices is just the tip of the iceberg). Still, a lot of people seem shocked that I could own a house in as nice a community as Naperville, Illinois for more than 14 years and end up selling it for less than I paid. Here are all the reasons why.

The Illinois Exodus is real

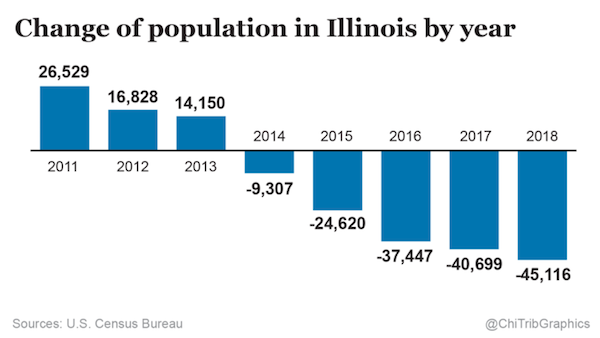

It’s now five years into the Illinois Exodus, and the state’s population losses are growing. We can debate whether that will continue (I think it will), what the causes are, and just how serious an issue it is: “as serious as a heart attack”, according to the editorial board of Chicago’s newspaper-of-record, the Chicago Tribune. Regardless, population loss does reduce the overall demand for housing. For those who remember the supply and demand equation from high school economics (do they even teach this anymore?), reduced demand leads to lower prices.

The U.S. Census Bureau says the Illinois Exodus is real

Death by property taxes in Illinois

Again, we can debate whether property taxes are unsustainably high in Illinois, and whether they are contributing to the Illinois Exodus (I’m in the yes on both camp). But what’s not really debatable is that high and rising property taxes reduce the amount of money that buyers can pay for a property. What matters to most buyers is their monthly payment: mortgage interest plus property taxes plus principal reduction. If more money has to go towards property taxes and/or mortgage interest, less is available to put towards principal. That means that buyers can’t afford to pay as much for houses, and prices must fall to meet the buyers. Naperville isn’t a bad off as Harvey, Illinois, but property taxes are high and rising.

Loss of suburban corporate jobs in Chicagoland

I’ve blogged about this trend: tech companies, and many other companies, are moving their headquarters to downtown, which in Illinois means Chicago. McDonald’s exited a huge campus in Oak Brook for the West Loop, Conagra moved into the Merchandise Mart and forced their Naperville office employees to commute downtown, and Motorola (what’s left of the cellphone handset business) departed Schaumburg, to cite a few of the bigger names. What’s a positive for Chicago is a negative for the suburbs, however, and a net breakeven at best for the state (usually large companies downsize a bit as they relocate).

Additionally, many of the tech companies in the Naperville area have fallen on hard times since we moved there in 2005. What’s left of Lucent, which became part of Alcatel and then Nokia, is a tiny fraction of what it once was; ditto for Tellabs, which used to be a billion-dollar company, and the company I used to work for, Westell. There’s a lot of vacant corporate office space in the area.

Downtown Naperville appeals to two types of buyers: folks who work in Chicago and can commute downtown by train, and folks who work in the nearby suburbs. When the suburban corporate jobs disappear and Chicago employment remains steady, it reduces the overall number of potential buyers and hence demand.

Bought near the peak

I had to buy during the inflation phase of the nationwide housing bubble in early 2005 because I had relocated to the Chicagoland area. I was certainly aware of the bubble at the time, and always thought I had bought a few years before the peak of the bubble in 2008. But according to an unnamed source more knowledgeable than myself, in our particular neighborhood prices peaked in 2006, flattened out, and have in general been going down ever since. The neighborhood hasn’t recovered from the bursting of the housing bubble, and is unlikely to ever recover, if the Illinois Exodus continues.

Unfair property tax assessment

I never bothered comparing my property tax bill to my neighbors’ bills (hint to neighbors: you can do so right here) until I listed it for sale. While I owned the house the assessment would go up every year, the amount due would go up every year, and I’d buck up and write a larger check to the “State” every year. As it turned out, because other houses in the neighborhood have sold recently at lower prices than originally paid, the houses with more recent sales have been assessed at a meaningfully lower rate per square foot than my house. To cite just one example, a house four doors away built roughly when my house was built, with similar construction quality and almost 20% more square footage, has a lower property tax bill than my house (that house was sold in 2017 at a loss). Neighbors who have been in your house for many years: your property tax assessment is probably too high and not reflective of today’s market reality.

I should have realized this problem years ago. Appealing a property tax assessment, however, is not an easy process, and may expose a homeowner to one of the most corrupt aspects of Illinois politics (see forthcoming blog post on Illinois property tax scams).

New versus used

Would you prefer to buy a new car, or that same car when it is 14 years old? You’d almost certainly only be willing to buy the 14 year-old car if it was priced lower than the new car. The same applies to houses. Houses last longer than cars, but it’s a fact of life that an older house is going to have systems within it (appliances, the air conditioning, the furnace, the roof, etc.) which are nearer the end of their useful lives than a brand new house. So you should pay less for it, all other things being equal.

Our house was brand new when we bought it. It wasn’t a teardown because there was never another house on that property, but it was in an area where they are still doing teardowns: replacing 100 year-old bungalows with brand new larger homes. This brand new housing reduces the value of the existing homes: buyers who can pay top dollar buy the new houses, and the rest of the housing stock moves down a little in price over time. This is actually a good thing: it’s why new construction at the high end of the market ultimately benefits all buyers, by increasing the housing stock and making all other housing a little cheaper. It’s very difficult to explain this to someone who rebels against new “unaffordable” high-end housing going up, but again you have to believe in the supply-and-demand equation.

Don't ask me why 7th Avenue doesn't cross Washington Street to the west

Bad reputation for our block due to flooding issues

Sorry, neighbors, but the word is definitely out about the flooding problems at the lower end of our block.

Illinois is very flat. As a kid our family would drive through the Chicagoland area on our way to visit my grandparents who lived in Milwaukee. I can remember my younger brother asking our father, “Dad, how does the water know which way to flow?”, and Dad having to stumble through an explanation. It’s so flat that engineers were able to reverse the flow of the Chicago river many years ago. It’s a problem for the entire area.

It’s also been a problem on our street, where the water flows down a slight grade to the lower end of the street where there is a storm drain that is supposed to shuttle the water elsewhere. During periods of heavy rain in the past, that storm drain would back up and a small pond would form. When we first saw this happen we jokingly called it “Lake Webster”, since our house was on Webster Street. It wasn’t much of a joke to the people on whose property Lake Webster formed, because their basements flooded. Over the years the city has made multiple attempts to improve the drainage. I haven’t seen Lake Webster form for several years, but who can really say if the problem has been fixed?

I can truthfully say that our old house has never, ever been affected by the city’s storm drainage issues, and that Lake Webster, when it has formed, has never come close to our property. It is hard to imagine how much rain would need to fall in order for it to do so; certainly a Hurricane Harvey-like storm, with four feet of rain in a few days would do it, but Chicago is much further inland than Houston and as a result does not get huge amounts of rain from the remnants of hurricanes that finally blow that far north.

Explaining this to skeptical buyers, however, was a big challenge. Our neighborhood is in such a desirable location, within walking distance to schools, shopping, and (more importantly) the Naperville commuter train station, with its rush hour express trains to downtown Chicago that whisk you to Union Station in 30 minutes, that there are buyers interested in moving into the neighborhood who are watching every new listing that goes up. I had a small degree of hope that we’d be able to quickly sell to one of these buyers.

Prospective buyers did pounce on our listing, and we were bombarded with questions about flooding. I answered every question truthfully, and even got down to nitty-gritty details of explaining how the property is graded, and how and where the water flows downhill during heavy storms. In the end, none of these prospective buyers moved forward with an offer, probably because of skepticism about the answers (who can say for sure?). We also got some questions about the driveway, including several who expressed skepticism that the driveway to the garage in back was wide enough to accommodate a car. I felt like answering that one, “Yeah, you’re right, it’s only wide enough for bicycles, but you can store 30 bicycles in the three car garage.” I couldn’t overcome the skepticism of these prospective buyers: they lost out on a perfectly fine house, and we lost out on potential buyers for our property. That reduces the demand in the supply and demand equation.

A quirk of the map and the street numbering system

The previous issue might not have been so bad if but for a quirk in the way that the neighborhood streets were laid out more than 100 years ago. In particular, our house was the last house on our side of the street at the higher-in-elevation end of the 600 block of North Webster Street before you get to 8th Avenue. There is no 7th Avenue in this small section of the Naperville street grid. The cross street at the lower end of Webster Street is 6th Avenue, so all the house numbers are in the 600s. Furthermore, for some reason the house numbers increment slowly along the block. Had this not been the case, and had 7th Avenue been part of the street grid in our neighborhood, our house number would probably have been something like 786 N. Webster Street. Instead it was 656, which makes it sound like it is right in the middle of the street that has the flooding issue. One more perception issue to overcome.

A city house, 'cause Chicago is, you know, a city

Not a farmhouse

Trust me, I’m almost completely clueless when it comes to trends. I was drawn to our house because I thought it was beautiful, classically-styled (a side hall Colonial), solidly built, and because it was almost completely sided in brick, which is low maintenance and can withstand the harsh upper Midwest winters. However, as my wife and others have pointed out to me, at this moment in time it is almost the exact opposite of what is trendy, which is the white-painted, wood-sided farmhouse, promoted by two people I’d never heard of before named Chip & Joanna Gaines.

The farmhouse style certainly doesn’t appeal to me. Evidently it does appeal to many of today’s buyers because so many new homes are being constructed in that style, in both our old Naperville neighborhood and our new neighborhood in the desert Southwest, for that matter. White paint will show dirt and marks more than any other color of paint, but that’s just my practical, left-brained side coming out. I guess they aren’t teaching The Three Little Pigs in kindergarten any more, because any kid who learned the lessons in that story would realize that a house made of sticks is not as durable as a house made of bricks. But again that’s just my practical side coming out: a house is more of an emotional purchase.

Will the farmhouse trend run its course? Will these farmhouses being constructed today look incredibly dated a decade or more from now and be forever linked to this moment in time, in the same way that bell-bottomed jeans are linked to the 1970s? I think so, but again I am clueless when it comes to trends. In the meantime I had to sell a non-farmhouse in the midst of the farmhouse craze.

Given all these issues, plus a desire to be rid of the house so that we can free up the money for other uses, I’m actually happy with the price we got. Given the overall trends in Illinois I doubt the house will end up being a good investment for the new owners, but as I said a house shouldn’t be viewed as an investment. It’s just a very nice place to live.