|

|

posted: November 19, 2021

tl;dr: “Almost no one” predicted inflation at the beginning of the COVID-19 endemic, but I did...

One of the fun things about economics is that it is the one field in which Nobel Prizes are awarded where I, or any lay person, can often be smarter than someone who has a Nobel Prize. That could never happen in physics, chemistry, medicine, or even literature. But it's pretty easy to be smarter than Nobel Laureate Paul Krugman when it comes to economics.

Krugman admitted this week that he "got inflation wrong". I nailed it back on May 30, 2020 when I wrote this in a post entitled I sold my bonds:

I see many inflationary pressures as a result of the COVID-19 pandemic. The Federal Reserve and the federal government are working together to create huge amounts of money. The federal budget deficit this year will be the largest in decades. The Federal Reserve is making unprecedented moves into the bond market, buying up trillions of dollars of assets. There is pressure to do even more, to send money to state and local governments that won’t be able to pay back their own bondholders without drastic budget cuts. Meanwhile, GDP will fall significantly this year, so we’ll have more money chasing fewer goods.

Kudos to Krugman for admitting he was wrong

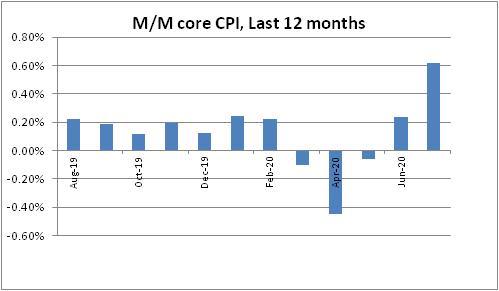

At the time, in May of 2020, we were still in the initial deflationary period of the COVID-19 endemic, as companies lowered prices to move inventory while demand was collapsing due to lockdowns which kept shoppers at home. The Consumer Price Index (CPI) went down, not up, in May 2020, as this graph shows. So I daresay it was a bold call to predict inflation when we were still in deflation. Also in that post I nearly called the very peak of the bond market, so I also put my money where my mouth was.

Where did Krugman go wrong? Krugman is very focused on the demand side of the economy, and doesn't seem to realize that prices can rise when demand falls. The supply side is where the bigger problems are because of the endemic, and we are still far away (years) from things settling down to whatever the new equilibrium is going to be. With all the monetary and fiscal stimulus applied to the demand side, what we ended up doing was generating huge demand during a severe supply shock. Of course prices are going to rise.

For now, unless there is a pullback, we’re in the positive feedback loop of printing more money to deal with rising prices that was a primary characteristic of the Weimar hyperinflation, as described in the book When Money Dies. This could reverse, especially if the federal government becomes split between the parties, leading to gridlock in our system of state-directed capitalism. However, there was a lot of fiscal stimulus and monetary expansion even before control of the Presidency and Congress flipped political parties in January of 2021, and few in D.C. want a recession, so I think the monetary and fiscal stimulus will continue.

I’m in the “almost no one” camp

Where do we go from here? Krugman has stated that he is a member of “Team Transitory”, which believes the inflation we’re experiencing now will quickly diminish as supply chain kinks get worked out.

I’m a member of “Team Persistent”, as I believe we’re a little more than one year into what will be another decade-long (at least) great American inflation, such as we went through in the 1940s and in the late 1960s to early 1980s. Just like the COVID-19 pandemic never went away and instead became an endemic, many of the changes wrought by it will also become permanent, and those changes, for the most part, are inflationary.

The endemic caused some workers to retire early, and others to refuse to re-enter the workforce because of concerns about the virus or difficulties with childcare: parents have learned that the schools and daycare centers they relied upon in the past to take care of their kids can be shut at a moment’s notice. This results in a permanently smaller workforce, which means fewer goods and services being produced. The endemic laid bare the downsides of global supply chains and has caused companies to reverse course and onshore production to the more regulated, higher cost U.S.A.

There will be continued fiscal spending to help people who are suffering, and to deal with the higher costs that inflation produces. This will necessitate more monetary expansion to fund the fiscal spending and to keep nominal interest rates low and real interest rates negative. The government actually needs the inflation to inflate away the debt that has been accumulated at the government, corporate, and personal levels. Ultimately I think there will be a monetary reset as the U.S. dollar loses some or most of its use as a global reserve asset, and stops being used as a unit of account for pricing things globally, such as oil.

Our monetary authority, the Federal Reserve, can’t fight inflation. The economic recovery is too fragile. There is too much debt in the system that will never be repaid. There are too many zombie companies (see AMC), municipalities (see Chicago), states (see Illinois), and arguably, the country as a whole. All these entities would go bankrupt if they lose the ability to borrow more money at artificially low interest rates. If the Fed stops buying bonds and raises interest rates, it would likely tip the economy into a recession. It may go into recession anyway, as the economy still hasn’t sufficiently restructured for the endemic COVID-19 reality. For example there are still a lot of companies holding onto expensive commercial real estate, expecting that their workforces will someday return to them, as we approach the second anniversary of the onset of the endemic.

But I may be completely wrong. After all, I don’t have a Nobel Prize in economics like Paul Krugman does 😉

Related post: How to create inflation

{kind=link}