|

|

posted: July 23, 2021

tl;dr: A market that is not allowed to function eventually ceases to be a market...

The bizarre happenings in the bond market are a primary reason why I sold my bonds last year.

The perversities include:

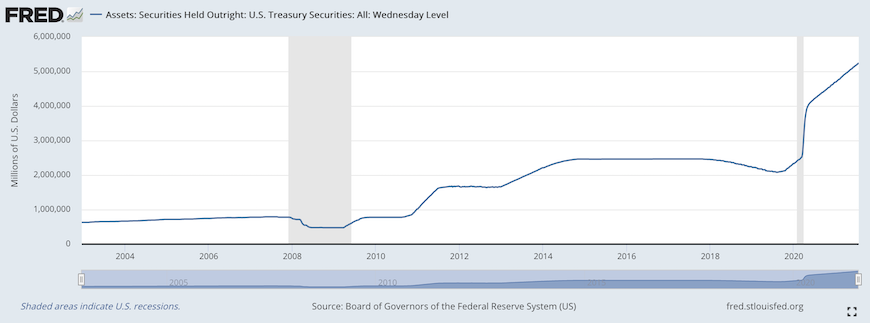

These are all strong signs that the bond market is anything but a free market. It has a high degree of central planning: the Federal Reserve both sets the price for short-term money (interest rates) and has purchased trillions of dollars of U.S. Treasuries, which soaks up a good portion of the available supply. This increases prices and decreases interest rates for all durations of bonds. While the Fed is focused on controlling the prices of government bonds, its actions also affect the prices of corporate bonds; in fact, that is part of the Fed’s intent, to make corporate borrowing cheaper and to stimulate the economy.

How high will this graph go over the years ahead?

The Fed doesn’t care what price it pays for the bonds it buys, since it manufactures the money it pays out of thin air. The resulting inflation in the money supply, the inflation in other asset prices, and now the consumer price inflation that we’re experiencing are all brushed aside. I believe the Fed is on a mission that seems very similar to what was done after World War II: suppress interest rates so that real interest rates are negative for years, and accept the resulting price inflation, to inflate away the debt that we’ve accumulated as a country.

How all this ends is a topic of heated debate among investors and the focus of one of my favorite podcasts, The End Game, which is one of the podcasts produced by Grant Williams. When I was younger there were investors known as bond vigilantes, who would bet against government bonds in inflationary periods such as this. The bond vigilantes are nowhere to be seen now, and may have been smothered by the sheer volume of bonds being purchased by the Fed. Other investors, fearing asset bubbles elsewhere, may be happy to hold bonds and lose some purchasing power each year, thinking that those losses will be capped by the Fed, which will prevent nominal bond prices from falling (and nominal interest rates from rising) too far, for fear of bankrupting the U.S. government.

As time goes by and the pandemic-triggered inflation I predicted persists, I think we’re witnessing the end of the bond market, similar to what has happened in Japan. In the end, there is no bond market: there is just the Fed, and some other investors who are willing to hold bonds at whatever price the Fed sets. Bond prices and interest rates don’t move much at all: they just stay in whatever narrow range near zero that the Fed sets, as this Reuters article about the sleepy bond market in Japan describes. Why trade something whose price can hardly move? The Fed, like its Japanese counterpart the Bank of Japan, ends up owning most of the bonds, and its balance sheet balloons. Feliz Zulauf predicts exactly this on my favorite episode of The End Game, which is definitely worth a listen.

Maybe the Fed, like the Bank of Japan, expands its bond buying into corporate bonds and even stocks. After all, wouldn’t it be nice if the major ups and downs in the stock market came to an end? There’s already ample evidence that the Fed reacts to major drops in the stock market, as it did again at the onset of the pandemic. Surely the Fed can set better price ranges in the stock market than the Robinhood meme stock traders driving GameStop stock through its major ups and downs, right?

The downside of eliminating the bond market, and perhaps the stock market someday, is that you eliminate price discovery and the subsequent reallocation of capital. Instead of those functions being performed by millions of market participants acting independently, it is performed by a much smaller number of smart central planners in the Eccles Building in Washington, D.C. Whatever you call this system, it’s not free market capitalism.

Related post: Look out below!